By Emmanuel Nsamba, Ph.D.

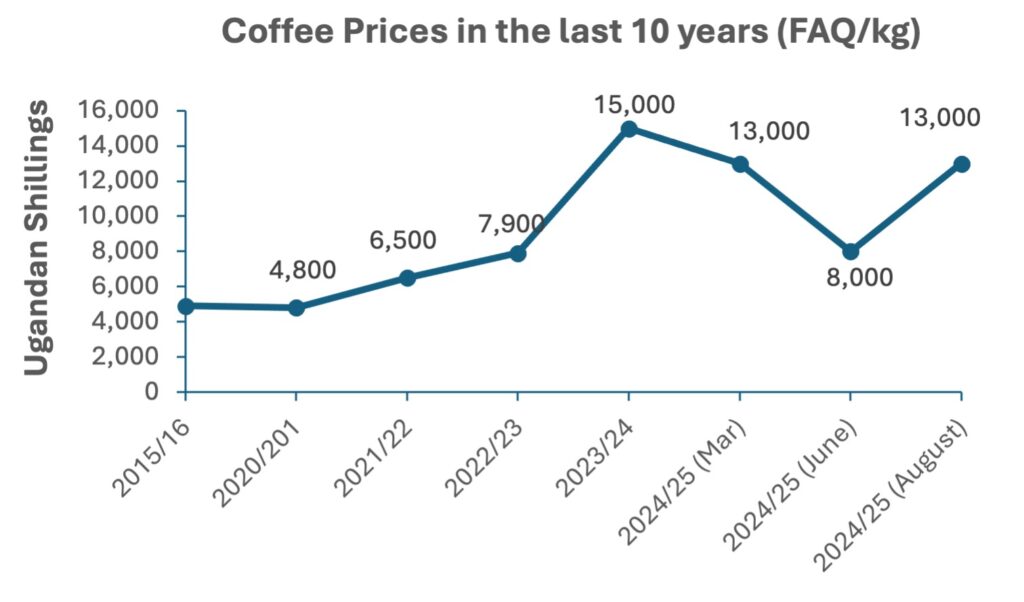

The recent coffee price fluctuations have shaken farmers who have invested heavily in commercial plantations, leaving many prospective growers questioning whether to enter this once-lucrative enterprise. The 2024/25 production season has been particularly turbulent, with prices swinging dramatically three times in just six months. In June, coffee (FAQ) prices plummeted 40-50% from UGX 15,000 to UGX 8,000 per kilogram, a devastating blow that left farmers reeling (Figure 1).

Mr. Guweddeko, who manages 200 acres of commercial coffee, exemplifies this struggle. When prices began dropping in mid-May, he held onto 15 tons of dried coffee, expecting a temporary dip. Instead, steady declines forced him to sell at a 50-million-shilling loss. His story resonates with thousands of farmers across Uganda who watched their anticipated profits evaporate.

Figure 1: Coffee price trends in Uganda

When Global Giants Stumble, Opportunities Arise.

To understand Uganda’s coffee opportunity, we must look to Brazil, the world’s coffee goliath that produces nearly 40% of global supply. In July 2021, Brazil’s coffee-producing regions were devastated by the worst frost in 27 years, followed by severe drought conditions that persisted through 2022. The frost alone destroyed an estimated 10-12 million bags of coffee, with some farmers losing 90% of their harvest. The impact was immediate and dramatic. As Brazil’s production capacity crumbled, global coffee futures soared nearly 20%.

The drought continued to ravage Brazil’s primary coffee states, Minas Gerais and São Paulo, creating creating supply shortages that rippled across international markets. This crisis opened the door for African producers, particularly Uganda. As the world’s second-largest robusta producer, Uganda was perfectly positioned to fill the supply gap. Coffee prices in Uganda more than doubled from UGX 6,500 in 2021/22 to UGX 15,000 in 2023/24, a 130% increase that transformed the agricultural landscape.

The Golden Rush: Uganda’s Coffee Boom (2021-2024)

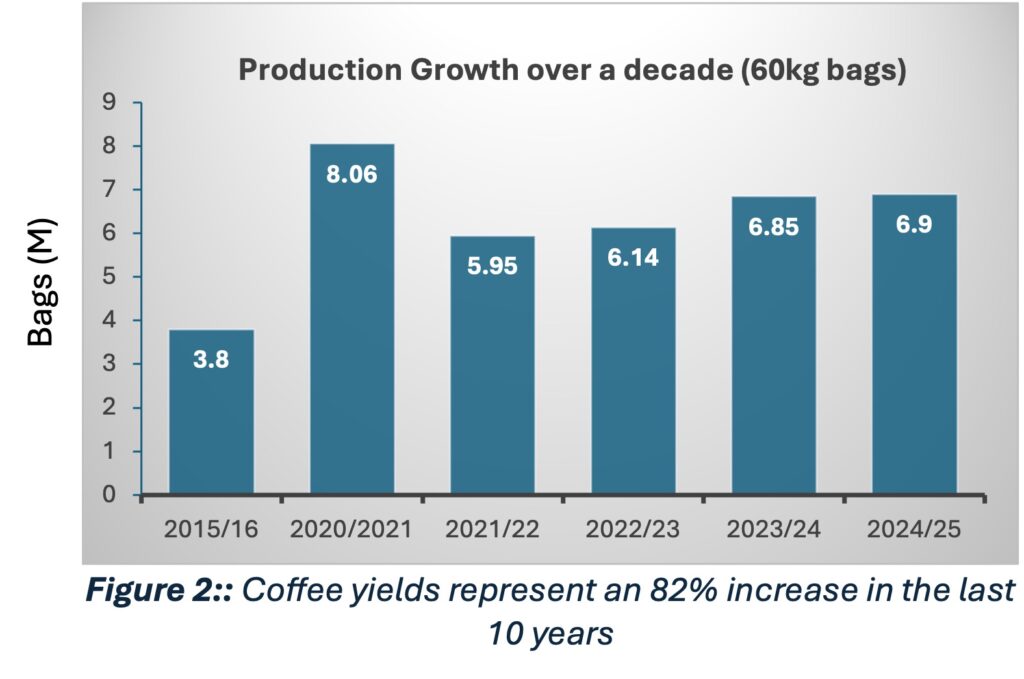

The price surge created an unprecedented coffee boom across Uganda. Production increased by 15%, reaching new heights as farmers expanded existing plantations and new investors entered the market (Figure 2). The enterprise attracted people from all walks of life, including professional workers, civil servants, and entrepreneurs – all seeking to capitalize on coffee’s golden moment.

In Central Uganda, the Buganda Kingdom launched the “Mwanyi Terimba” (Everyone should grow coffee) campaign, which received an overwhelming response. Families that embraced coffee farming experienced transformative changes: steady income flows, children attending better schools, new homes, and improved living standards. The commodity became more than just a crop; it became a pathway out of poverty for rural communities. The boom extended beyond traditional coffee regions. Northern Uganda, historically not a coffee-growing area, witnessed significant plantation development as farmers diversified from subsistence crops to this lucrative cash crop.

Market Volatility Tests Farmer Resolve

However, success bred its own challenges. As Brazil’s weather improved and production began recovering, global supply projections shifted dramatically. Coffee markets, being globally integrated, responded swiftly to news of Brazil’s recovery. Ugandan coffee prices dropped by an average of 45-50% from their 2023/24 peaks (Figure 1).

The timing couldn’t have been worse. This price collapse coincided with controversial government restructuring that saw the Uganda Coffee Development Authority (UCDA) merged with the Ministry of Agriculture, Animal Industry and Fisheries (MAAIF). Many farmers, lacking insight into global market dynamics, viewed this as government interference rather than natural market correction. Conspiracy theories about government interference included alleged attempts to manipulate prices and monopolize the industry, all which reflected farmers’ frustration and lack of understanding about global coffee markets. Under immense pressure, MAAIF released a press statement with explanations about international price drivers, although trust remained fragile among coffee-growing communities.

For average farmers and prospective investors, the question became urgent: Is coffee still worth the investment?

The Numbers Don’t Lie: Why Coffee Still Reigns Supreme

Even considering a scenario where coffee prices dropped 40-50% to their pre-Brazilian crisis levels and remained there indefinitely, my cost-benefit analysis reveals coffee’s enduring superiority among Uganda’s cash crops. The data is compelling:

Table 1:: Cost Benefit analysis of Uganda’s major traditional cash crops1

| Crop | Annual Production Costs (UGX ‘000) | Annual Gross Revenue (UGX ‘000) | Net Profit (UGX ‘000) | Profit Margin |

| Coffee2 | 1800 – 2000 | 55000 – 60000 | 53200 – 58000 | 95% |

| Maize3 | 600 – 800 | 1500 – 2000 | 900 – 1200 | 60% |

| Beans4 | 360 – 520 | 1600 – 4000 | 1240 – 3480 | 82% |

| Bananas5 | 280 – 370 | 2000 – 4800 | 1700 – 4450 | 88% |

| Cocoa6 | 3500 – 4000 | 48000 – 57000 | 44500 – 53000 | 92% |

1Note: These estimates are based on farmers with existing land under production, excluding land acquisition/hiring, clearing, or new seedling costs for perennial crops. References are provided.

My analysis reveals that coffee generates net profits of 53-58 million UGX per acre annually, dramatically outperforming all alternatives. Specifically, Coffee produces 12-48 times higher net profits than maize (900-1,200K), 13-47 times higher than beans (1,240-3,480K), and 12-34 times higher than bananas (1,700-4,450K). Only cocoa approaches coffee’s profitability range (44.5-53 million UGX), serving as the second most highly valued crop. However, cocoa’s ecological growth restrictions prevent broad countrywide adoption, while coffee edges out cocoa in optimal land utilization; it’s not strictly a shade crop and can be successfully intercropped with major cash crops including bananas and cocoa itself.

Additional Benefits of Coffee sector: Coffee’s supremacy in Uganda’s agricultural sector rests on five fundamental pillars that no other crop can match. First, its profit generation capacity is unparalleled – delivering 12-48 times higher returns than traditional crops and maintaining 95% profit margins even during market downturns (Table 1). Second, coffee offers exceptional land efficiency through successful intercropping with bananas, beans, and cocoa, maximizing productivity per acre. Third, its geographic adaptability spans Uganda’s diverse ecological zones, from traditional growing regions to emerging northern areas, providing universal farming opportunities. Fourth, coffee demonstrates remarkable market resilience with established international demand channels and its position as Uganda’s second-largest export commodity ensuring consistent buyer interest. Finally, its scalability advantage allows both smallholder and commercial farmers to succeed, making it accessible across all farming scales while maintaining profitability thresholds that dwarf competing crops.

Brazil’s Troubles Continue: Uganda’s Sustained Advantage

Recent developments suggest Uganda’s coffee advantage may be more sustainable than initially expected. As I write this article, Brazil faces new frost warnings that threaten the 2026 harvest. Weather patterns indicate continued volatility in Brazil’s coffee-producing regions, with climate change making extreme weather events more frequent and severe.This ongoing instability in the world’s largest coffee producer creates sustained opportunities for reliable suppliers like Uganda. In the latest press release by MAAIF, Coffee prices have already begun recovering, rebounding to UGX 13,000-14,000 per kilogram by August 2024, approaching their earlier highs.

Long-term Market Dynamics Favor Uganda: Two powerful market forces position Uganda for sustained coffee sector dominance in the global arena. Climate stability emerges as Uganda’s strongest competitive weapon; while Brazil grapples with increasingly unpredictable frost, drought, and extreme weather events, Uganda’s equatorial location provides the consistent growing conditions that international buyers desperately need for supply chain security. This reliability advantage coincides perfectly with accelerating global coffee consumption, particularly in emerging markets like China. Most critically, as major coffee buyers actively pursue supply diversification strategies to reduce Brazilian dependency, Uganda’s proven production consistency and improving quality standards position the country as an indispensable strategic partner rather than merely another supplier option.

Strategic Recommendations for Farmers

Coffee wilt disease resistant (CWDr) coffee cuttings ready for planting

Current market conditions present the optimal entry point for strategic coffee investment, not retreat. The fundamentals driving coffee’s superior profitability remain structurally intact; global supply constraints, growing demand, and Uganda’s competitive advantages have not disappeared with temporary price corrections. Smart farmers should recognize these price dips as cyclical market adjustments that create expansion opportunities at reduced establishment costs, while positioning their operations for the next inevitable price surge. The mathematical reality is unequivocal: even at current reduced prices, coffee generates profit margins and absolute returns that no alternative crop can approach (Table 1), making this the ideal moment to establish or expand coffee enterprises before the next supply crisis drives prices higher.

For prospective farmers considering entering the coffee business, success hinges on making informed decisions and seeking proper technical guidance from the outset. Coffee farming requires specialized knowledge about variety selection, proper establishment practices, and long-term farm management – areas where expert advice becomes invaluable for newcomers to the enterprise. Bakugu Agricultural Technologies Limited (Bagritech.com), certified by the Ministry of Agriculture, specializes in producing Coffee Wilt Disease Resistant (CWDR) coffee cuttings, including advanced KR varieties, with lines; KR-1, KR-3 and upto to KR-10, tailored to farmer preferences. Beyond quality coffee seedlings supply, Bagritech offers comprehensive farm management services covering everything from farm planning and budgeting to land preparation, planting, and early coffee management through the fruiting stage.

Beyond coffee, Bagritech Nurseries is certified by the Food and Agriculture Organization (FAO) to produce cocoa, fruit, and various tree seedlings including Pine, Eucalyptus, etc. With five years of specialized experience in the Nursery business and farm management, Bagritech provides the technical foundation new farmers need to transform their agricultural aspirations into profitable realities. For consultation and quality planting materials, contact: info@bagritech.com

Conclusion: Coffee’s Crown Remains Secure

The recent price volatility, while challenging, doesn’t diminish coffee’s fundamental position as Uganda’s most profitable crop. The numbers are undisputable: even during market downturns, coffee generates superior returns compared to traditional alternatives. Further, Brazil’s ongoing weather challenges, combined with growing global demand and Uganda’s improving quality standards, create a compelling long-term outlook. The farmers who weathered this year’s price storms are already seeing recovery, with prices rebounding toward previous highs.For those questioning whether coffee remains worth the investment, the evidence is clear: Coffee is still Uganda’s gold and now may be the perfect time to stake your claim.

Coffee’s crown remains secure, and strategic investors who recognize this moment as opportunity rather than crisis will reap the greatest rewards.

References:

2. Profit Margins on Maize Production. https://naads.or.ug/profit-margins-on-maize-production/

3. Return to investment in coffee production: Uganda’s highest value crop. https://bagritech.com/return-to-investment-in-coffee-production-ugandas-highest-value-crop/

4. Beans Sector Strategy – Uganda. https://www.casaprogramme.com/wp-content/uploads/CASA-Uganda-BeansSector-analysis-report.pdf

5. ANALYZING AGRICULTURAL SCIENCE AND TECHNOLOGY INNOVATION SYSTEMS: A case Study of Banana sub-sector in Uganda. http://repository.ruforum.org/system/tdf/Banana%20ASTI%20case%20study.pdf?file=1&type=node&id=31298

6. Rising cocoa price: Can Uganda do more than export raw beans: https://www.monitor.co.ug/uganda/business/commodities/rising-cocoa-price-can-uganda-do-more-than-export-raw-beans-5153860

Author:

The author holds a Bachelor of Science in Agriculture with a major in Economics and comes from a coffee-growing family that used coffee proceeds to fund his education.